Why Generosity Should Be Part of Your Financial Plan

Learn why generosity should be part of your financial plan. Discover how thoughtful planning, biblical stewardship, and strategic giving can help you align your finances with your faith and aim to create a lasting impact.

When most people think about financial planning, they think about saving for retirement, reducing taxes, or growing their investments. Those are all important goals, but there's another conversation that's just as important: how you plan to give.

For many families, generosity is a core value. Yet it's often treated as an afterthought, something that's considered only when there's extra money available or at the end of the year when tax planning comes into focus.

At Triune Financial Partners, we believe generosity shouldn't sit on the sidelines of your financial plan. It should be part of the conversation from the beginning.

Generosity Starts with Purpose, Not a Dollar Amount

One of the biggest misconceptions about generosity is that it's something you do once you've reached a certain level of financial success.

In reality, generosity is less about how much you have and more about how intentionally you steward what you've been given.

At Triune, that perspective is rooted in the belief that everything we have ultimately belongs to God. Rather than viewing money as something to accumulate, we see it as a resource to steward wisely, caring for our families, preparing for the future, and making a meaningful impact in the lives of others. That philosophy has shaped Triune since its founding and continues to guide the way we help clients make financial decisions today.

Planning Can Give You the Confidence to Give

One of the greatest benefits of having a financial plan is clarity.

When you understand where you are today and where you're headed, generosity becomes less of a guessing game and more of an intentional decision. Financial planning can help you better understand your available resources and priorities.

Instead of asking, Can we afford to give? you begin asking better questions:

How much should we set aside for charitable giving each year?

How do we balance generosity with retirement savings and other goals?

How can we involve our children in giving?

What kind of legacy do we want to leave?

A thoughtful financial plan helps answer those questions in the context of your entire financial life, giving you confidence that your generosity aligns with both your values and your long-term goals.

Giving Wisely Can Increase Your Impact

Generosity isn't only about your willingness to give. Understanding various options for giving can make a huge difference and can help you make informed decisions about your charitable goals.

For example, if you have appreciated investments in a brokerage account, the use of a Donor Advised Fund may provide potential tax advantages depending on your individual circumstances.

Contrary to what many people realize, a Donor Fund isn’t just for ultra-high net worth individuals. It can work with annual giving budgets as low as $5,000.

In addition to Donor Advised Funds, there may be strategies that make your giving more efficient, including:

● Incorporating charitable giving into your estate plan.

● Coordinating charitable gifts with retirement income when appropriate.

These aren't one-size-fits-all solutions, but they're examples of how financial planning can support generosity in practical ways.

Generosity Can Bring Clarity to Financial Decisions

One of the most rewarding things advisors often see is that generosity influences more than charitable giving.

When people intentionally make giving part of their financial plan, it often changes how they think about spending, saving, and investing as well.

That's because they've already answered an important question:

What is our money ultimately for?

Once that purpose becomes clear, financial decisions tend to become simpler. Rather than chasing more for the sake of more, families are able to make choices that reflect their priorities and the life they want to build.

As Triune often says, planning isn't simply about accumulating wealth. It's about aligning your resources with what matters most. That planning-first philosophy can help people move from financial complexity to greater clarity and confidence.

A Financial Plan That Reflects Your Values

Every financial plan tells a story. It reflects what's important to you, what you're preparing for, and the legacy you hope to leave behind.

At Triune, we believe generosity deserves to be part of that story. Whether you're giving to your church, supporting a nonprofit, helping your children, or investing in your community, your financial plan, we believe, should make room for the things that matter most.

When generosity is woven into a thoughtful financial plan, it becomes more than an occasional act. It becomes an intentional expression of your values.

If you'd like to build a financial plan that reflects both your goals and your faith, we'd love to start the conversation. Our team is here to help you create a plan that aims to bring clarity, confidence, and purpose to every financial decision.

This material is provided for informational and educational purposes only and is not intended to constitute investment, tax, legal, or accounting advice. The information presented may not be applicable to every individual’s circumstances, and you should consult with your qualified financial advisor, tax professional, or legal advisor before making any financial decisions. Any references to tax considerations, charitable giving strategies, or financial planning concepts are general in nature and should be evaluated based on your specific situation.

Is Your Retirement Plan Truly Serving Your Employees?

Learn what strong fiduciary oversight looks like for 401(k) and 403(b) plans. Discover how proactive governance, fee transparency, and employee-focused planning help organizations can support their people.

The retirement plan you offer says something about your organization’s values. When designed thoughtfully, it supports your team’s future while reflecting a culture of stewardship and care.

For business owners, nonprofit leaders, churches, and professional practices, sponsoring a retirement plan comes with real fiduciary responsibility. But fiduciary oversight does not have to feel intimidating or overly legalistic. At its core, prudent plan governance is simply about having a thoughtful process to ensure your plan is well-run and truly serves your employees over time.

As Geoff Huber, CFP® of Triune Financial Partners explains:

“One of the best measures of successful fiduciary plan governance is making sure that on a consistent, intentional, proactive basis, a partner is pulling the right levers to help support better outcomes for their employees over time.”

Healthy retirement plans are designed to help support employees as they prepare for their future. Here’s how your organization can make sure it’s pulling those “right levers.”

The Fiduciary Blind Spots Many Organizations Miss

Some employers assume their retirement plan must be working simply because nobody is complaining. In reality, many organizations operate for years without fully understanding whether the fees are competitive or if employees are benefiting from the plan design.

Geoff sees this often. “They don’t know what it costs,” he said. “They don’t know what it should cost. There’s no defined service model.”

Sometimes leaders say: “Oh yeah, we have a guy. He comes out when we call him.” But strong fiduciary oversight is proactive.

Healthy plans typically include:

Clearly defined decision-making roles

Precise, customized, modernized plan design

Regular plan reviews with documented notes and meeting minutes

Ongoing fee benchmarking

Institutional-style investment options, including managed portfolios

Reviews of investments and plan performance

Evaluation of provider relationships

Consistent communication with employees

Monitoring regulatory and compliance changes

Without these habits, retirement plans can drift into neglect, even when leaders genuinely care about their people.

Why “Set It and Forget It” Can Become Risky

One of the most dangerous assumptions in retirement plan management is believing that a plan can stay healthy indefinitely without regular review.

The retirement landscape changes constantly. Fees evolve, regulations shift, employee expectations change, and technology improves. What worked five or 10 years ago may no longer serve employees well today.

Fees are one of the clearest examples.

Geoff often compares retirement plan pricing to cell phone companies. New customers are constantly offered competitive deals while long-term customers continue paying higher prices unless someone actively benchmarks costs and renegotiates.

Many providers - especially insurance companies - use asset-based pricing structures, meaning fees rise automatically as plan balances grow. A plan that once seemed reasonably priced can become unnecessarily expensive over time if no one is reviewing it proactively.

In addition to fee-creep, operational mistakes can happen too. Contribution errors, payroll reconciliation issues, compliance oversights, or missed rule changes may go unnoticed for years without proper oversight. That is why fiduciary governance requires consistent attention and independent review.

Compliance Alone Is Not The Full Picture

A retirement plan can technically meet legal requirements while still falling short of serving employees well. From an employee’s perspective, the experience of the plan matters just as much as (or maybe more than) compliance. As Geoff puts it: “You can have a compliant plan without your employees getting any advice or any attention.”

Are your employees getting the most out of your organization’s retirement plan?

Do employees understand the plan?

Do they know how to participate?

Are they receiving education and guidance?

Are investment options thoughtful and aligned with their needs?

Does the plan feel usable and accessible, or confusing and overwhelming?

Strong plans focus not only on administration, but on employee engagement outcomes.

Well-run plans may support employees through features such as:

Automatic enrollment features

Auto-increase contribution strategies

Roth contribution options

Employee education meetings

Personalized guidance

Transparent communication

Investment options aligned with employee values and goals

Geoff shared that employee education efforts can be very effective:

“We often see employee meetings result in increased participation or contribution changes.”

Fiduciary Responsibility Is Really About Stewardship

For many organizations, especially faith-based businesses and nonprofits, fiduciary oversight is a leadership responsibility in addition to a legal responsibility.

Under the Employee Retirement Income Security Act (ERISA), fiduciaries are expected to act in the best interests of plan participants. But beyond regulations, there is a deeper reality: Retirement plans impact real people, real families, and long-term financial security. Caring faithfully for the people entrusted to your leadership means stewarding your retirement plan well.

A Better Retirement Plan Starts With a Better Process

At Triune Financial Partners, we believe retirement plans work best when they are approached intentionally, relationally, and proactively.

That means:

Planning before products

Transparent fiduciary guidance

Ongoing plan oversight

Thoughtful employee education

Regular benchmarking and reviews

A focus on long-term employee outcomes

As Geoff says: “Nothing bad ever happens when you spend time with people.”

That philosophy shapes how Triune partners with organizations every day. We come alongside business owners, nonprofit leaders, churches, and professional practices to help build retirement plans that are clear, well-governed, and aligned with what matters to you most.

The information in this material is provided for informational and educational purposes only and should not be construed as investment advice or a recommendation to take any specific action. Retirement plan services and investment advisory services are offered through Triune, an SEC-registered investment adviser. All views and opinions are subject to change without notice and may not reflect the views of all personnel at the firm. Information discussed is based on current and historical data and may not reflect future results. There is no guarantee that any strategies discussed will be successful or that objectives will be achieved. Investing and retirement plan participation involve risk, including possible loss of principal. Plan design and fiduciary practices are subject to applicable laws and regulations, which may change over time. Clients should consult with their advisor or legal counsel regarding their specific situation. Certain information contained in this material may be derived from third-party sources. While believed to be reliable, Triune does not guarantee the accuracy, completeness, or timeliness of such information and it should not be relied upon as investment advice.

Money Talks: Steps Toward Financial Harmony in Marriage

Struggling with money in your marriage? Learn how Triune helps couples work toward financial alignment through shared priorities, communication, and proactive planning.

We’ve all heard the statistics. In marriages that don’t work, money is too often the root cause. Over a period of time, husbands and wives who aren’t on the same page financially will gradually drift from each other. Discord begins to grow as they continue moving in different directions. And one day, they look up and wonder: How did we get ourselves into this mess?

It’s an all too common issue in our mile-a-minute world. But that’s why we’re here. At Triune, we believe there’s hope for every couple to live in financial harmony, as long as you’re willing to take the first step.

The Root of the Issue

You won’t find a husband and wife anywhere who think that money isn’t important. But most of the time, it doesn’t feel like the most important thing right now. Life is busy. Both spouses are spending their time and energy on their career or their family (or both). Usually, the thought is, “We know we need to get our finances figured out, but we’re busy. We’ll get to it when we have time.”

Unfortunately, with that mindset, the decision of when to “figure things out” is often taken out of a couple’s hands. Some kind of negative life or health-related event happens, and suddenly, they’re needing help. Oftentimes, they’re forced to be reactive instead of proactive, making financial decisions out of stress and anxiety, which can easily lead to more tension in a relationship.

The other dynamic that’s almost always present when a married couple delays talking about money is that one spouse ends up handling all the financial decisions. This is a normal dynamic within marriage—one spouse is more skilled, interested, or opinionated in financial matters, so they naturally take on most or all of the financial responsibility. The problem is, that leaves the other spouse without a voice. And when both spouses’ voices aren’t present in the conversation, there’s almost no chance that they’re on the same page.

All of this can contribute to an unbalanced, reactive financial reality for many couples today. However, there is a more intentional approach that may help couples build a healthier financial relationship over time.

A Better Way Forward

Anxiety and stress are natural human experiences, but God doesn’t intend for us to live in a constant state of stress and anxiety. His promise to us is peace, strength, comfort, and guidance, even in the hardest moments of our lives. And that’s possible, even in our finances.

When we wait to prioritize our finances until life forces us to, that can lead to trouble. But when we choose to be proactive instead of reactive, everything changes. And a great way to do that is to find a financial advisor who knows you, understands your life, and can walk alongside you as a married couple to help you make good decisions proactively.

We start with discovering shared priorities. Our financial advisors help husbands and wives get on the same page with their financial priorities, sometimes for the first time ever. What are your goals? What matters most to you, both now and in the future? These priorities don’t have to be written in stone, and they can shift as time passes and life happens. But a great first step is to sit down and agree on your priorities alongside an advisor who can help you stay aligned to them in real life.

Aligning on shared priorities leads to decision clarity. When you’re working with an experienced financial advisor who understands your priorities and shares your beliefs and worldview—that God is our provider, that He owns it all, and that our job is to be good stewards of what He’s given us—it can help couples feel more confident making financial decisions.

Staying aligned on priorities and decisions over time requires ongoing communication. We believe successful couples are intentional about finding time once or twice a year to sit down with their financial advisor, who is able to advocate for them and help them think well. When we set aside time to think well, it shapes our perspective. And when your long-term perspective is better, your short-term decisions will be, too.

The Triune Approach

At Triune, we see ourselves as partners and advocates for our clients.

Our goal is to be partners in conversation with every client who walks through our doors. Our job isn’t to lead with solutions, but to lead with questions that will help husbands and wives find clarity and harmony. We’re here to guide and help in the conversation, but we’re not here to tell you what to do.

As advocates, our goal is to advocate for both spouses in the conversation, but especially the one who enters the conversation with the least interest and, most likely, the least input. One important way couples can work toward financial harmony is if both the husband and wife have an equal voice. This doesn’t mean a wholesale role reversal, it means that in these conversations, both spouses’ voices carry equal weight. Many clients leave our conversations feeling like they’re genuinely interested in this conversation for the first time ever.

Our experience allows us to help husbands and wives work through common problems (if you’ve been through it, someone else probably has too, and we’ve probably worked with them on it!). And the relationships we form with our clients allows us to tailor our interactions to their priorities, goals, and values.

If you’re ready to take the first step toward financial unity as a married couple, we’re ready to join you as advocates and partners. Reach out today to start the conversation.

This material is provided for informational and educational purposes only and should not be construed as investment, legal, tax, or accounting advice. All opinions are subject to change without notice. Investing involves risk, including the loss of principal. Financial planning strategies discussed may not be appropriate for every individual or couple. Individuals should consult with their financial, legal, or tax professionals before making any financial decisions.

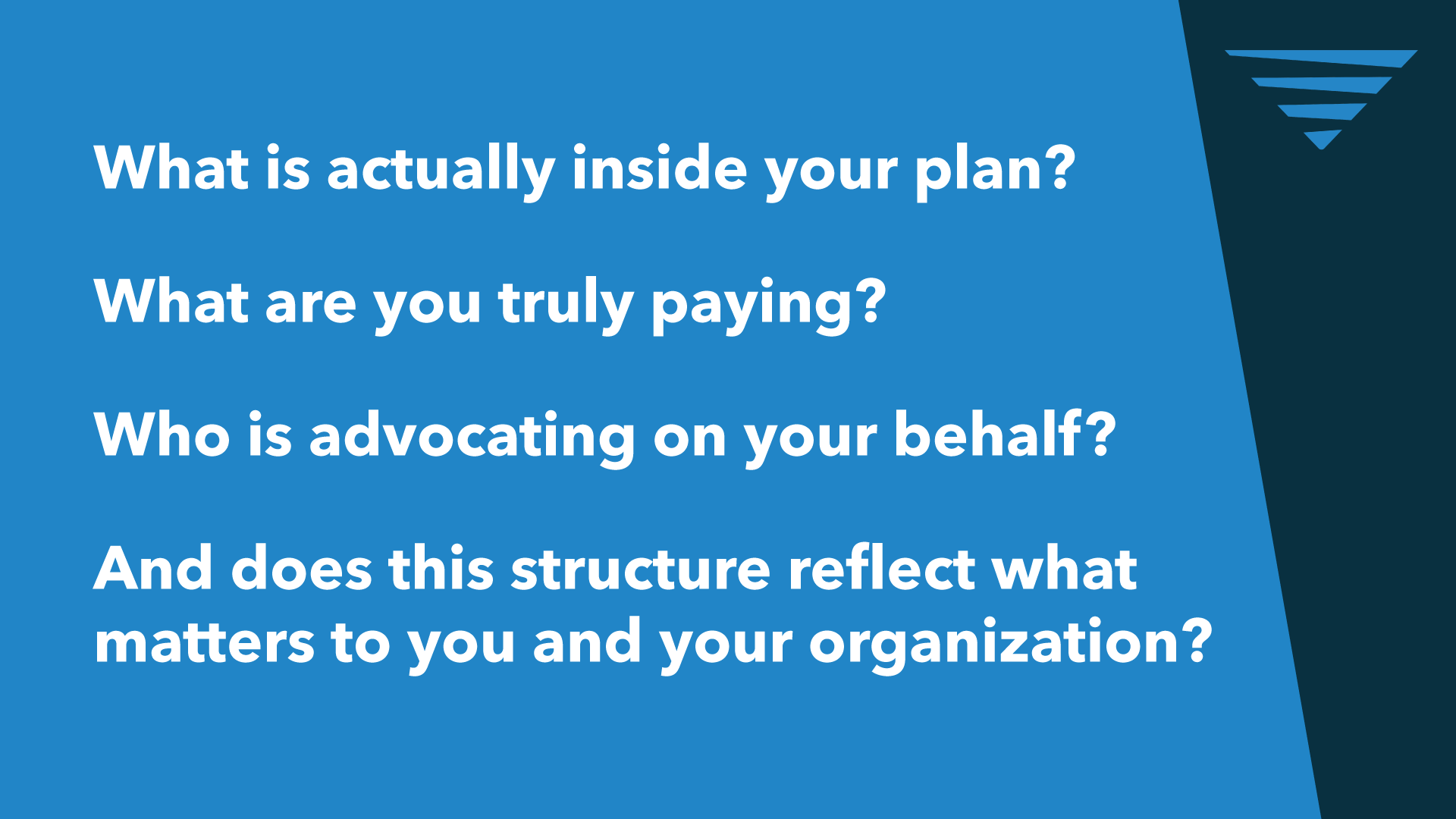

The Question Most People Never Ask About Their Retirement Plan

Are your investments aligned with your values? Learn how your workplace retirement plan may be investing your money.

Most people are familiar with workplace retirement plans like 401(k)s and 403(b)s.

At a high level, they are simple: you contribute a portion of your paycheck, your employer may contribute as well, and over time those dollars are invested with the goal of supporting your future. They are designed to help individuals and families build long-term financial security.

But underneath that simplicity is something more complex and significant.

Those contributions are not sitting idle. They are being invested into global markets, into funds, and ultimately into real companies across the economy. Which means a workplace retirement plan is not just a savings tool. It is an investment engine. And that leads to a question most people have never been asked:

What is that engine actually fueling?

The Question Almost No One Is Asking

According to Triune advisor Geoff Huber, this conversation is nearly absent in the workplace retirement space.

* “The next time that I bring up faith-based or values-based investing with somebody… and they say, yeah, we were just talking about that with our advisor the other day, that’ll be the first time.”

That should give us pause.

We are talking about one of the largest pools of long-term capital in a person’s life, and yet most participants and many leaders have never been asked to consider what sits underneath it.

Not out of neglect. More often, out of assumption.

The Reality Beneath the Surface

A workplace retirement plan can feel abstract. Numbers on a screen. Percentages. Growth charts. But the underlying reality is very concrete.

As Geoff explains, “When you put that money in your account… you’re buying a proportional interest in several hundred, if not several thousand different companies.”

That means every contribution is not just saving. It is participation. Participation in businesses. In industries. In decisions being made far beyond your line of sight. So the question becomes unavoidable:

If you could clearly see everything you own, would you still be comfortable owning it?

This Is Not About Perfection. It Is About Stewardship.

Faith-based and values-based investing is often misunderstood. It is not about achieving a flawless portfolio. That does not exist.

Geoff is clear about that: “It’s not a perfect science… I can never say we’re going to be 100% perfect all the time.”

The real issue is not perfection. It is intentionality.

Ignoring the question entirely is a decision. Engaging it thoughtfully is stewardship.

For individuals of faith, or organizations with a defined mission, this becomes even more meaningful. Because alignment is not just a financial concept. It is a reflection of what you believe responsibility looks like.

For years, the industry operated on a simple assumption: If you care about values, you give up performance. That assumption shaped behavior. It discouraged questions. It kept many from even exploring alignment. But the data has moved.

As Geoff put it, “The generally accepted wisdom was… choose your values or performance… that’s no longer the case… there’s no discernible difference.”

No guarantees. No promises. But the premise has shifted. Which means we believe the real barrier today is no longer performance. It is awareness.

Why Most People Can’t Fix This on Their Own

Here is where the conversation gets more practical and more serious. Most employees cannot meaningfully change this on their own.

Why?

Because they are choosing from a pre-built menu.

And as Geoff explains, “If it isn’t done on the plan level, it’s virtually impossible to do on the employee level.”

This is a leadership issue.

The business owner.

The CFO.

The executive director.

The board.

The investment committee.

They are not just selecting funds. They are defining the options available to every employee and every family connected to that plan. That responsibility deserves more than autopilot.

The Quiet Cost Most Plans Ignore

While values often go unexamined, fees are frequently misunderstood. And the impact is not small.

Geoff described it plainly: high fees are like “starting the 100-meter dash 30 meters behind the rest of the field.”

That gap compounds over time. What makes this more concerning is how often it goes unchecked. Many plans are set up once and left alone. Meanwhile, the plan grows, and so do the dollars being paid in fees.

Without intentional oversight, overpayment can persist for years.

What High-Level Guidance Actually Looks Like

This is where experience matters. Not product selection. Not surface-level advice.

Real guidance starts by asking better questions. The kind most people have never been asked.

Geoff emphasized that many clients have never even considered these questions until they are asked.

From there, the role of a firm like Triune is not to force conclusions. It is to bring clarity, provide context, and help leaders and families make informed decisions.

Because alignment is rarely obvious. It has to be uncovered.

When Was the Last Time You Took a Real Look?

Most people can answer that question quickly. Or they cannot answer it at all.

Geoff described the typical responses:

Some say “never.”Some say “maybe 10 years ago.”A few say “recently.”

The reality is, the marketplace has changed. Investment options have evolved. Fee structures have compressed. The conversation around values has matured. But many plans have not kept up.

A Second Opinion Is a Structured Review Process.

At Triune, the S.O.S. (Second Opinion Service) provides a structured review.

Not to create friction. Not to replace relationships unnecessarily.

But to bring clarity to four critical areas:

Fees

Performance

Plan design

Alignment with values and goals

These are the same core areas fiduciaries are expected to monitor and evaluate on an ongoing basis. Informed decisions require visibility. And visibility rarely happens by accident.

This Is About More Than a Plan

Workplace retirement plans are often treated like administrative necessities.

They are not.

They are long-term financial engines.They are leadership decisions.They are expressions of care for the people who depend on them.

Your people are not participants. They are families, futures, and stories in progress. We help you steward that responsibility with clarity and care.

A More Honest Starting Point

If you have never asked what your plan truly reflects, you are not behind. You are simply at the beginning of a better conversation. Start there.

When was the last time you really looked under the surface?

And if the answer is unclear, a second opinion is not a risk.

It is, in our opinion, a wise next step.

This material is provided for informational and educational purposes only and should not be construed as investment advice or a recommendation to buy or sell any security. Views and opinions expressed are those of the author and may not reflect those of Triune. Information referenced in this material may include third-party sources believed to be reliable, but Triune does not guarantee the accuracy, completeness, or timeliness of such information and makes no representation regarding its suitability for any particular purpose.

*The views expressed are those of Geoff Huber, a representative of Triune. This statement is not a client testimonial. No compensation was provided for this statement.”

5 Ways Fraudsters May Lure Victims Into Scams Involving Crypto Asset Securities

Fraudsters often use innovations and new technologies to perpetrate investment scams, and this has been the case with crypto asset securities-related investments. While federal and state regulators continue to bring enforcement actions in this space, recovering money from the fraudsters can be difficult because it can be challenging to trace and recover funds.

Content shared from the Security and Exchange Commission (SEC). The SEC’s Office of Investor Education and Advocacy is issuing this Investor Alert because fraudsters continue to exploit the popularity of crypto assets to lure retail investors into scams. Crypto assets may include assets commonly referred to as cryptocurrencies, crypto, coins, and tokens.

Fraudsters often use innovations and new technologies to perpetrate investment scams, and this has been the case with crypto asset securities-related investments. While federal and state regulators continue to bring enforcement actions in this space, recovering money from the fraudsters can be difficult because it can be challenging to trace and recover funds. For example, fraudsters can use technology to obscure their identities or hide the trail of funds using crypto assets. Recovering your investment from a crypto asset-related scam can also be difficult because fraudsters can quickly send your funds overseas.

Fraudsters use a variety of techniques to convince investors to hand over their hard-earned money. Here are five things you should watch out for to avoid losing your money to a scam involving crypto assets.

Fraudsters Connect With You on Social Media Platforms or Through a Supposedly Accidental Text Message, and Then Gain Your Trust.

Fraudsters may initiate contact with potential victims on social media platforms — including professional networking, dating, and messaging websites/apps — or through unsolicited text messages. They may pretend to be an old friend or claim to have contacted you accidentally. The fraudster may quickly move communications with you away from the initial platform. The fraudster may then initiate a friendship or romantic relationship with you to build trust and convince you to invest your money before disappearing with your funds. These relationship confidence scams are sometimes referred to by a term that is as unpalatable as the fraudsters’ conduct — “pig butchering scams.”

One way this type of scam can play out is that after a fraudster has established an online relationship with you, the fraudster may claim to know about lucrative investment or trading opportunities, including investments involving crypto assets. The fraudster may even indicate that a relative or friend works at a financial firm or is an “insider” and therefore is able to provide trading information. The fraudster may direct you to a legitimate-looking (but fake) website or to a widely-used app that can be downloaded from a well-known app store, make it look like you have profited, and even allow you to withdraw a small amount of “profits,” further gaining your trust. The fraudster may then ask you to invest larger sums of money. When you want to withdraw your funds, the fraudsters often come up with an excuse why that is not possible, or they may tell you for the first time that you must pay more to cover fees or taxes. Frequently, there is no way you will recover your investment or any “profits” so paying additional funds only causes you to lose more money.

For anyone you have met solely online or through an app:

Do not make investment decisions based on their advice or solicitation. Note that fraudsters may direct you to get Bitcoin at a Bitcoin ATM (or kiosk) or through a crypto platform in order to make investment deposits, and then tell you where to send that Bitcoin. Keep in mind that an investment may not be legitimate if you are required to pay for it with crypto assets.

Do not share with them any information relating to your personal finances or identity. Do not given them anything like your bank or brokerage account information, tax forms, credit card, social security number, passport, driver’s license, birthdate, or utility bills.

Fraudsters Exploit the Hype Around Emerging Technologies Such as Artificial Intelligence (AI).

Fraudsters may use the growing popularity of artificial intelligence (AI) as a hook for luring investors into crypto asset securities-related investments. It might seem exciting to invest in crypto asset-related investments that have a connection to AI, but be careful. Fraudsters often use the hype around new technological developments, like emerging AI technologies, to lure investors into scams. Fraudsters may use catchy AI-related buzzwords and make claims that you will make a lot of money when their only intention is to steal your money. They may claim to deploy bots that use AI to find the best crypto asset-related investments.

Fraudsters also may use AI technology itself to produce realistic looking websites or marketing materials to promote investment scams, including crypto asset-related investment scams. Similarly, they may use AI technology to create “deepfakes” — cloning, altering or faking voices, images, and videos to deceive investors. They may even create deepfakes of celebrities, government officials, or your loved ones in order to gain your trust or to convince you to send funds.

Fraudsters Impersonate or Exploit Trusted Sources.

Be aware that communications — including phone calls, voicemails, text messages, messages via social media, emails, letters, and certificates — may falsely appear to be from official U.S. government sources, including the SEC. If you receive a communication that appears to be from the SEC, do not provide any personal information until you have verified that you are dealing with someone from the SEC, and not an impersonator.

AI technology has made it even easier for fraudsters to impersonate government agencies, organizations, and individuals in luring investors into scams. Fraudsters may even impersonate your friends or family members using AI technology to create deepfakes. They also may hack your friends’ or family members’ social media accounts, and then post or send messages pretending to be from them. For example, they may post that your friend or family member has become a crypto asset expert and seeks friends to join in trading or investing.

Even if you are certain that an investment pitch is coming from a friend or family member, keep in mind that they may have been fooled into believing that the investment is legitimate when it is not. Sometimes fraudsters target communities or groups by recruiting leaders or others to pitch an investment without them knowing that the “opportunity” is a scam.

Fraudsters May Pump Up the Price of a Crypto Asset and Then Sell at Your Expense.

Fraudsters may conduct pump-and-dump schemes with crypto assets, including so-called “memecoins” that refer to popular culture or internet memes. For example, fraudsters may create a memecoin and then tout it on social media – sometimes in what they refer to as a “pre-sale” – to get others to buy and “pump” up, or increase, its price. Then the promoters or others working with them “dump,” or sell, before the hype ends, profiting from the pumped up price. Typically, after the promoters sell and take their profit, the price decreases rapidly, and everyone else who bought the tokens loses most of their money. Never make investment decisions based solely on information from social media platforms or apps.

Fraudsters Demand Additional Costs That They Falsely Claim Will Allow You to Withdraw From Your Account, or to Recover Losses.

In investment scams, including ones that involve crypto asset securities, fraudsters may demand that you pay additional costs, fees, or taxes to withdraw money from your account. This is an example of an advance fee fraud, where investors are asked to pay a bogus fee upfront before receiving anything. For example, fraudsters may falsely tell you that your account has been frozen by a regulator or because a regulator is investigating your account. They may ask you to pay a large deposit, fee, or sum of taxes to unfreeze your account. If you pay, however, you are unlikely to receive your initial investment and will also lose the additional payment.

Another way fraudsters may trick you into paying additional costs is by telling you they “mistakenly” deposited money into your account and ask you to refund the money. They never actually put money in your account – it’s just a ploy to convince you to give them more money.

Fraudsters also may target you if you already have lost money or crypto assets due to bankruptcy or a scam. They may ask you to send them the private key to access your crypto assets, or to put in additional money or crypto assets, offering to “help” you recover what you lost. In reality, if you pay, you likely will not get back what you put in and will instead have been scammed again.

***

Don’t get caught up in the fear of missing out (FOMO) on a purported investment opportunity that seems new or “cutting-edge.” If you are considering an investment involving crypto asset securities, look out for the tactics described above and other warning signs of an investment scam.

5 Simple Steps to Take BEFORE You Sell Your Veterinary Practice

Owning a veterinary practice can be a fulfilling and financially rewarding venture. However, it also comes with its unique set of financial challenges. In this blog, we'll explore the critical role of personal financial management for veterinary practice owners and how your personal finances can significantly impact the success of your practice.

We recently spoke with Kayla Donovan about her thoughts on selling a veterinary practice. Below, she's shared an overview for vet practice owners.*

Owning a veterinary practice can be a fulfilling and financially rewarding venture. However, it also comes with its unique set of financial challenges. In this blog, we'll explore the critical role of personal financial management for veterinary practice owners and how your personal finances can significantly impact the success of your practice.

As a veterinary practice owner, your personal financial stability is closely intertwined with the health of your business. By understanding and managing your personal finances effectively, you not only ensure your own financial well-being but also lay a solid foundation for the growth and prosperity of your practice.

1. Establish Financial Goals

Setting clear financial goals is the first step towards securing your financial future. As a veterinary practice owner, it's crucial to have both short-term and long-term goals for your personal finances. Short-term goals may include paying off debt, building an emergency fund, or saving for a family vacation. Long-term goals might involve retirement planning, investing in real estate, or funding your children's education.

By defining these goals, you create a roadmap for your financial journey. These goals will serve as a source of motivation and direction, helping you make informed financial decisions.

2. Plan for Cash Flow

Managing cash flow is paramount for personal financial stability and the success of your veterinary practice. To ensure you have enough funds to cover both personal and professional expenses, consider creating a detailed cash flow plan. This plan should account for your practice's income and expenses as well as your personal financial obligations.

A well-structured cash flow plan allows you to allocate funds efficiently, ensuring that you can reinvest in your practice, pay yourself a fair salary, and maintain a healthy work-life balance.

3. Manage Debt

Debt management is a critical aspect of personal finance. High-interest debts can quickly erode your financial security and put your practice at risk. It's essential to develop a debt repayment plan that prioritizes paying off high-interest debts first while maintaining necessary business and personal expenses.

Consider consolidating high-interest debts into lower-interest options, such as a business loan or personal line of credit. This can reduce the financial burden and help you regain control of your finances.

4. Plan for Retirement

Planning for retirement is often overlooked by many veterinary practice owners. However, it's a crucial step in securing your financial future. Working with a financial advisor who specializes in retirement planning can help you create a tailored retirement plan that aligns with your personal goals and the financial needs of your practice.

By contributing to retirement accounts and investments, you not only secure your own retirement but also ensure the continued success of your practice, as a well-prepared owner can transition out of the business smoothly when the time comes.

5. Seek Professional Counsel

Aside from a personal Financial Planner, there are two other relationships you must have before selling your veterinary practice.

A Trusted CPA (ideally one who specializes in veterinary practices)

An experienced Practice Broker

The value of an experienced Practice Advisor can’t be discounted… here are a few things they’ll help you to consider before putting your business on the market.

Preparation is Key: Start planning early with your broker to maximize offers. They'll help construct a roadmap, ensure clean financials, and offer guidance on making your practice more marketable.

Timing Matters: Discuss your personal and professional timing with your advisor, aligned with market trends. Timing the sale right can significantly impact offers and opportunities.

Know Your Worth: Work with your advisor and accountant to determine your practice's value and uncover growth opportunities. Early valuation helps shape your roadmap.

Unlock Higher Offers: Utilizing a broker not only ensures higher offers but also streamlines the sales process, allowing you to focus on running your practice stress-free. Don’t leaving money on the table by trying to do it on your own!

Conclusion

In summary, mastering your personal finances as a veterinary practice owner is not just about securing your own future; it's about ensuring the continued success and growth of your practice. To thrive in the veterinary industry, follow these five key money moves:

1. Set clear financial goals for both the short and long term.

2. Develop a cash flow plan that balances personal and professional expenses.

3. Prioritize debt management and consolidation to reduce financial stress.

4. Collaborate with a financial advisor to create a solid retirement plan.

5. Aligning yourself with the right trusted advisors can make all the difference in successfully selling your practice.

By taking action now to improve your personal finances, you are setting the stage for a prosperous future for both you and your veterinary practice. Your financial stability and success go hand in hand, and with careful planning and dedication, you can achieve both.

ABOUT TRIUNE FINANCIAL PARTNERS

Triune Financial Partners is committed to empowering people with life-changing financial counsel. Triune is an independent firm that values clarity, simplicity, and transparency. We're a fiduciary, which means we always put our clients' interests first. In addition to Financial Life Planning for individuals and families, we also serve 100+ businesses, churches and nonprofits to craft powerful 401(k) and 403(b) plans for their organizations. Whether you're working with one of our Financial Life Planners or setting up a 401(k) plan for your organization, Triune is here to help you thrive financially.

Interested in working with us? Get in touch here.

*The content shared in this blog post includes material and viewpoints from a collaborating entity, Kayla Donovan of Evo Transition Partners. Please note that the business operations, opinions, and perspectives presented by the collaborator are solely their own and do not necessarily reflect the views, policies, or endorsements of Triune Financial Partners, LLC (Triune). Triune does not warrant or assume any legal liability or responsibility for the accuracy, completeness, or usefulness of any information, product, or process disclosed by the collaborator. The inclusion of any third-party content does not imply endorsement or recommendation by Triune.

Building a Diversified Portfolio for Tech Workers in Uncertain Times

At Triune Financial Partners, we've seen firsthand the unique challenges tech workers face with concentrated stock positions. In this blog, we explore the importance of diversifying your portfolio.

Written by Brad Banowetz, Financial Planner

You know that feeling of hitting refresh on your browser and seeing your company stock soaring? That rush of excitement, the sense of being part of something groundbreaking, and the tantalizing whisper of early retirement. For many of us in the tech world, it's a familiar experience, and one that often comes bundled with a generous package of company stock options. But let's be honest, that feeling can also be a double-edged sword. While riding the rocket ship of a fast-growing tech company can be exhilarating, there's also often a hidden danger lurking beneath the surface: an overly concentrated portfolio.

At Triune Financial Partners, we've seen firsthand the unique challenges tech workers face with concentrated stock positions. As a former Tesla employee, myself, I understand the allure of riding the wave of a high-growth company. But as a financial advisor, I also know the importance of diversification – spreading your assets across different industries and asset classes to mitigate risk, weather market storms, and accomplish personal goals.

Why Diversify?

Imagine riding a unicycle down a winding mountain path. Every bump, every gust of wind threatens to throw you off balance. That's what a concentrated portfolio feels like in volatile markets. One bad turn for your company stock, and your entire financial future could be thrown into jeopardy.

Diversification is like riding a sturdy mountain bike. With multiple wheels and gears, you can navigate uneven terrain with greater stability and control. This doesn't mean abandoning your beloved tech stock entirely. It simply means allocating a portion of your wealth to other sectors, asset classes, and even geographically diverse investments.

The Challenges of Tech-Heavy Portfolios

Volatility: Tech stocks are notorious for their up and down cycles. While the potential for high returns is enticing, the potential for significant losses is just as real. A concentrated position amplifies this risk, leaving your financial wellbeing dangerously exposed to the fortunes of one company.

Lack of Income: Many tech companies prioritize reinvesting profits for growth rather than paying dividends. This means relying solely on stock appreciation for income in retirement can be risky. Diversifying into income-generating assets like bonds and dividend-paying stocks can provide a more stable financial cushion.

Overconfidence: Riding the wave of a successful company can breed overconfidence. Investors may underestimate the risks involved and neglect diversification, potentially setting themselves up for a rude awakening when the market inevitably changes.

Beyond the Numbers: Focusing on Your Goals

Financial planning is about more than just numbers on a spreadsheet. It's about understanding your goals and values to help craft a plan that leads you to achieve your financial dreams. This plan starts with understanding your current financial picture, looking at where you want to go, and taking steps to get you from point A to B. At Triune Financial Partners, we believe in a holistic approach, considering not just your investments but also your debt, spending habits, and long-term goals is the key to a successful financial future. Investing is just one piece of the puzzle.

It's common for advisors not focused on holistic planning to stop at the investment management part of diversification. This approach strictly looks at what you currently have in your portfolio and determines how much you need to sell based on what the suggested allocations typically look like – typically 5% to 10% of your net worth. For example, an individual with a $1M net worth, shouldn’t hold more than $50,000 to $100,000 in one stock. Working with an advisor that is only focused on your investment allocation will tend to lead you down a path of high tax implications and unclear direction on how to use the funds.

Building a Diversified Portfolio

At Triune, we focus on holistic planning which means your goals are what drives the rest of the plan. Instead of strictly looking at your investments as a percentage, we’ll help you identify where you’d like to go and how you can use your portfolio to get you there. From that point, we’ll then build out a plan based on your risk tolerance to help sell off portions of your concentrated portfolio to allocate it towards the proper asset. For example, if you want to carve off part to use for a house down payment in 5 years – that will get invested much differently than if you tell us you’d like to carve off a portion for your retirement in 30 years. This goals-based approach allows us to be intentional about where to park funds to make sure they are there when you need them.

Fortunately, there are effective strategies for tech workers to diversify their portfolios without sacrificing their belief in their company's future. Here are a few tips:

Set Goals: One size fits all approaches don’t work here. Your life is personal and involves short, medium, and long term goals. Each goal requires specific strategies and plans to accomplish.

Sell gradually: Selling a large portion of your stock all at once can trigger significant tax consequences. Consider a gradual divestment strategy, spreading out the sale over time to minimize tax impact.

Consider Tax Consequences: Understanding your income and the different tax implications of stock awards is important to minimizing the impact taxes have on your plans results. Implementing specific strategies can help reduce this burden even further.

Seek professional help: Navigating the complexities of portfolio diversification can be overwhelming, especially for busy tech workers. Consulting a qualified financial advisor can help you develop a personalized strategy that aligns with your goals and risk tolerance.

The Triune Difference

As an independent firm, we're not beholden to any specific products or financial institutions. We're free to prioritize your best interests and provide objective, unbiased advice. We also value clarity, simplicity, and transparency, ensuring you understand every step of the process.

Whether you're a seasoned tech veteran or a fresh-faced startup employee, remember, your financial future is not tied to the fate of any single company. Embrace diversification, and empower yourself to build a resilient portfolio that can weather any storm. At Triune Financial Partners, we're here to guide you every step of the way.

Contact us today to schedule a free consultation and take control of your financial future.

Remember, diversifying your portfolio is not about abandoning your dreams. It's about building a stronger foundation for achieving them.

ABOUT TRIUNE FINANCIAL PARTNERS

Triune Financial Partners is committed to empowering people with life-changing financial counsel. Triune is an independent firm that values clarity, simplicity, and transparency. We're a fiduciary, which means we always put our clients' interests first. In addition to Financial Life Planning for individuals and families, we also serve 100+ businesses, churches and nonprofits to craft powerful 401(k) and 403(b) plans for their organizations. Whether you're working with one of our Financial Life Planners or setting up a 401(k) plan for your organization, Triune is here to help you thrive financially.

Interested in working with us? Get in touch here.

Aligning Your Values & Your Money: Financial Wellness in the New Year

Aligning your values with your financial goals will help you to stay on track (or get back on track if you get knocked off), and will facilitate greater financial wellness along the way. Because as they say, it’s about the journey, not the destination.

The new year has begun, and like many of us, you have probably set a few New Year’s Resolutions. And like the majority of Americans, you will probably quit on your resolution within three months.

Womp womp.

Kind of a downer, right? We feel it, too.

But it’s the reality – many of us fail to stick to our goals, even when we have the best intentions.

And while we cannot give you advice on how to stick with your health goal, or help you read the 12 books you’ve committed to reading, we can help set you up for success with your financial goals.

One of the most critical steps to accomplishing your financial goals is ensuring they are aligned with your values… your “why”.

Aligning your values with your financial goals will help you to stay on track (or get back on track if you get knocked off), and will facilitate greater financial wellness along the way. Because as they say, it’s about the journey, not the destination.

So let’s dig in and discuss some of the fundamentals of financial wellness, and make a game plan for aligning your unique personal values with your money.

What is Financial Wellness?

Financial wellness goes beyond simply having enough money. It encompasses a holistic approach to managing our financial lives, taking into account our emotional, mental, spiritual and physical well-being.

Financial wellness is about having a sense of control over our finances. It is about knowing where our money is going and making conscious decisions about how we spend, save, and invest.

When we are financially well, we are not only focused on the present moment, though we are likely able to enjoy it more fully. We also have a long-term perspective and are able to make decisions that will benefit us in the future. We are able to set realistic goals and create a plan to achieve them. We are also able to navigate unexpected financial setbacks and make adjustments as needed.

The Connection Between Values and Money

Our values play a significant role in shaping our financial decisions. They serve as a compass, guiding us in determining what brings us joy, satisfaction, and fulfillment. By understanding our core values, we can make intentional choices that align with our beliefs and priorities.

Identifying Your Core Values

Take some time to reflect on what truly matters to you in life. What are the guiding principles that shape your decisions and actions? Is it family, adventure, health, spiritual growth, or contributing to a cause you believe in? Identifying your core values will help you align your financial goals with what you find most valuable.

How Values Influence Financial Decisions

Once you have a clear understanding of your values, you can start evaluating how they impact your financial decisions. For example, if two of your core values are "family" and "adventure", you could invest more thoughtfully in family vacations to make lasting memories. We like to refer to these investments as getting a "good return on life".

Steps to Align Your Values with Your Finances

Now that we understand the importance of aligning our values with our money, let's explore some practical steps to achieve financial wellness.

Evaluating Your Current Financial Situation

The first step is to evaluate your current financial situation. Take stock of your income, expenses, debts, giving and savings. This evaluation will provide a clear picture of where you stand financially and help you identify areas that may need improvement.

Setting Financial Goals Based on Your Values

Once you have a thorough understanding of your financial situation, it's important to set goals that align with your values. These goals can be short-term, such as paying off debt or saving for a vacation, or long-term, such as purchasing a home or planning for retirement. By setting goals that are meaningful to you, you are more likely to stay motivated and committed to achieving them.

Creating a Value-Based "Budget"

As you may have read before, we don't really believe budgets work. So we'll call it a Spending Plan. A spending plan is a powerful tool that can help you align your values with your finances.

As you create your spending plan, allocate your income to reflect your priorities. Consider how much you want to allocate to different categories such as savings, investments, travel, health, home improvement, giving, etc. This is often the first step to aligning your money with your values... in essence, you're "voting with your dollar"... and you're casting a ballot for the life you want to live.

Maintaining Financial Wellness Throughout the Year

Financial wellness is an ongoing journey. It requires regular check-ins and adjustments to ensure that we stay on track. Here are some tips to help you maintain financial wellness throughout the year:

Regular Financial Check-ins

Set aside time regularly to review your financial progress. Are you on track for what's most important to you? Use this opportunity to make any necessary adjustments or modifications to your financial plan.

Adapting Your Financial Plan as Your Values Evolve

Our values may evolve over time as we gain new experiences and perspectives. As your values change, it's important to revisit your financial plan and make adjustments accordingly. Regularly reassess your goals and ensure they continue to reflect what is important to you.

Overcoming Challenges in Aligning Values and Money

Aligning our values with our money is not always easy. There are often challenges that can hinder our progress. Here are some common challenges and strategies to overcome them:

Dealing with Financial Stress

Financial stress can make it difficult to align our values with our money. It's important to practice self-compassion and develop healthy coping mechanisms to manage stress. Seek support from loved ones, mentors or consider consulting a financial professional who can provide guidance and help you navigate difficult financial situations.

Balancing Multiple Financial Goals

It's common to have multiple financial goals that may sometimes compete with one another. When faced with competing goals, prioritize based on your values. It may be helpful to break down larger goals into smaller, manageable steps. By taking a systematic approach, you can make progress towards each goal while ensuring alignment with your values.

Conclusion

In conclusion, aligning your values with your money is a powerful way to achieve financial wellness. By understanding the concept of financial wellness, recognizing the connection between values and money, and taking practical steps to align your finances with your values, you can create a life that is both financially secure and meaningful. Remember, financial wellness is a continuous journey, so regularly revisit and adapt your financial plan as your values evolve. May this new year be an opportunity for you to align your values and money, bringing you closer to a life of fulfillment and satisfaction.

ABOUT TRIUNE FINANCIAL PARTNERS

Triune Financial Partners is committed to empowering people with life-changing financial counsel. Triune is an independent firm that values clarity, simplicity, and transparency. We're a fiduciary, which means we always put our clients' interests first. In addition to Financial Life Planning for individuals and families, we also serve 100+ businesses, churches and nonprofits to craft powerful 401(k) and 403(b) plans for their organizations. Whether you're working with one of our Financial Life Planners or setting up a 401(k) plan for your organization, Triune is here to help you thrive financially.

Interested in working with us? Get in touch here.

5 Powerful Reasons Business Owners Should Establish a 401(k) Plan

We’ve worked with hundreds of business owners and seen countless times the value of offering a retirement plan – not just for your employees, but for you. There are probably some benefits you aren’t aware of, so let’s dive into why offering a 401(k) plan will benefit you.

Saving for retirement is a no-brainer – at least, it should be.

But for some business owners, creating a 401(k) plan is not on their “to-do list.”

We’ve worked with hundreds of business owners and seen countless times the value of offering a retirement plan – not just for your employees, but for you. There are probably some benefits you aren’t aware of, so let’s dive into why offering a 401(k) plan will benefit you.

1. Retirement saving and investing.

This one seems obvious, but it’s worth mentioning.

Saving for retirement is an essential part of any Financial Life Plan. One of the most common ways–and first steps–is to contribute to your 401(k) plan. Studies suggest that you should save at least 15% of your gross earnings (depending upon life stage and goals) for retirement. The maximum contribution you can make in 2023 is $22,500, or $30,000 if you’re age 50 or older. You can choose if your contributions are either Pre-tax or Roth. Unlike IRAs, there are no income limits for Roth in a 401(k) plan, so even high-income earners have options.

When it comes to saving for retirement, the earlier, the better. For both you and your employees, the benefits of a 401(k) are unmatched when it comes to creating a strong plan for retirement

Read More: The Basics of Retirement Planning

2. Tax Planning

If you don’t currently offer a 401(k) plan, you might be missing out on some significant tax benefits.

Many small business owners overpay on their income taxes, but a properly designed 401(k) retirement plan can help you save money on taxes. Business owners get tax deductions for their pre-tax contributions, employer matching contributions, as well as plan expenses. Some of our clients choose to utilize al Profit-Sharing option in their plan.

Profit Sharing is a way to save up to $66,000 ($73,500 for those 50+) inside a properly designed 40(k) plan. The tax savings on that amount can be more than the contributions for employees. This means some of the money you were going to pay to the government in income taxes goes to your employees instead. Win / Win!

Let us help you determine if Profit Sharing is a good option for you based on your team’s specific demographics. A fiduciary like Triune will work closely with your CPA and a Third Party Administrator (TPA) to determine the right amount for you to put into a Profit-Sharing plan and maximize benefits.

You might be wondering the value of redirecting some of this money to your employees, and this leads directly into our next three points: Recruit, Reward, Retain.

3. Recruit

Offering a retirement plan option to your employees is a significant component of the total compensation package. In fact, many employees look for this specifically when seeking work.

So it’s become increasingly mainstream to offer a 401(k) plan with a robust matching formula. This can be used as a recruiting tool–and for smart business owners, marketing matching benefits is a key part of their recruiting strategy. Discretionary Profit-Sharing on top of matching, tied to a 6-year graded vesting schedule, can be the cherry on top!

4. Reward

Rewarding your employees is a key way to ensure their dedication to your business goals–and we’re not talking about pizza parties or “Casual Fridays.” Many employers choose to offer a 401(k) match to their employees, and some make a Profit-Sharing contribution at the end of the year. Some of our clients do this every year, while others choose to only enact Profit-Sharing if they have a really good year in business.

Creating targets that everyone can work toward together–and then rewarding your team for hitting them–is not just a great way to reward your employees, but to build a culture of team players.

5. Retain

By regularly rewarding your employees with meaningful incentives, you’ll retain them for longer than the average business owner.

Retaining employees longer than a year or two is challenging in this market. But most companies don’t offer a Profit-Sharing incentives–so this can make you stand out as an employer.

Of course, you’ll need to communicate the true value of what you’re offering to your team. If one of your 26-year-old employees gets an extra $2,500 into their 401(k) because everyone hit their targets and the company increased revenue, that could be worth up to 10X that amount by the time they retire.

Read More: Why You Need a Second Opinion Service For Your 401(k) Plan

Conclusion

If you’re a business owner ready to offer a 401(k) plan, please reach out to learn more about working with Triune. Many financial advising firms don’t have the capacity to personalize 401(k) plans and Profit-Sharing. We work closely with all our clients to custom design 401(k) plans specific to their needs. We would be honored to visit with you about your situation.

ABOUT TRIUNE FINANCIAL PARTNERS

Triune Financial Partners is committed to empowering people with life-changing financial counsel. Triune is an independent firm that values clarity, simplicity, and transparency. We're a fiduciary, which means we always put our clients' interests first. In addition to Financial Life Planning for individuals and families, we also serve 100+ businesses, churches and nonprofits to craft powerful 401(k) and 403(b) plans for their organizations. Whether you're working with one of our Financial Life Planners or setting up a 401(k) plan for your organization, Triune is here to help you thrive financially.

Interested in working with us? Get in touch here.

Is Too Much Cash a Bad Thing? An Analysis of the Pros and Cons

Is there such a thing as having too much cash? There can be. In this article, we'll take a closer look at the concept of "too much cash" and examine the pros and cons associated with holding excess funds.

It’s easy to assume there’s no problem with having a lot of cash on hand. After all, you do need to have cash on hand in many situations. Whether it's for paying bills, saving for goals, or simply having some extra spending money, cash is an essential part of our daily lives.

But is there such a thing as having too much cash? There can be.

In this article, we'll take a closer look at the concept of "too much cash" and examine the pros and cons associated with holding excess funds.

Btw… when we say “cash”, we mean the money you have in checking, savings or money market accounts.

Understanding the Concept of “Too Much Cash”

Before we dive into the pros and cons, let's first define what we mean by "too much cash.”

Essentially, this refers to a situation where an individual or business has more money on hand than they need for their immediate needs or planned expenses.

While having some extra cash can provide a sense of security and freedom, holding too much can lead to missed opportunities and other potential drawbacks

How Much Cash is Too Much Cash?

The answer to this question will vary depending on a number of different factors, including an individual's income, expenses, and financial goals.

Here’s an example for how we might determine this number for a Triune client:

Basic Situation

The client’s short-term needs include their emergency fund, travel, and a minor home improvement.

The client spends ~$7,500/mo on their lifestyle, plans to spend $10,000 on a home improvement project, and wants $5,000 for their travel this year.

Determining the Right Amount of Cash

$22,500 – Emergency Fund (this client is comfortable with three months’ lifestyle costs)

$10,000 – Home Improvement

$5,000 – Travel

Total Cash Needed = $37,500

If the client has cash above $37,500, then it should likely be put to better use (like paying down high interest debt or investing)

The Role of Cash in Personal Finance and Business

Cash is, of course, a tool that we use to purchase goods and services. However, it also provides a sense of security and flexibility.

Cash reserves can be used to weather unexpected financial setbacks or plan ahead for major expenses or goals. For businesses, cash is an important component of day-to-day operations, helping to fund growth and handle unforeseen expenses.

However, holding onto excess cash can have some downsides.

For example, if that cash is simply sitting in a low-interest savings account, it may not be earning as much as it could be. We see a Financial Life Plan in “time horizons”, and if the time horizon for your goal is within two years, then keeping it in savings (ideally a high interest account) is wise. But if you have cash you don’t really need for more than 2 years, then paying down debt more aggressively or investing the money is likely a smart move.

So while having some extra cash on hand can provide a sense of security and flexibility, holding onto too much can have potential drawbacks. Be sure to consider factors like interest rates, investment opportunities, and personal financial goals in order to determine the appropriate amount of cash to hold onto. And of course, you should always speak to your financial advisor about how much cash you need available for your lifestyle.

The Pros of Having Excess Cash

While holding too much cash can be ill-advised depending on your financial goals, there are certainly some benefits to having a solid reserve of funds on hand. Below, we’re sharing a few advantages to consider.

Financial Security and Emergency Funds

Perhaps the most obvious advantage of having excess cash is the sense of security it provides. By having a buffer of funds available, individuals and businesses alike can weather unexpected financial challenges without having to resort to taking on debt or selling off assets.

An emergency fund can cover expenses like medical bills, car repairs, or job loss without disrupting long-term financial plans or causing undue stress. In addition, having excess cash can provide peace of mind and reduce anxiety around financial uncertainty.

Flexibility in Decision Making

Cash reserves can provide a degree of flexibility when it comes to making financial decisions.

For individuals, this could mean being able to take time off from work without worrying about paying the bills, or having the funds to pursue a new hobby or interest. For businesses, a cash reserve could allow for more experimentation and risk-taking with new products or ventures.

Having excess cash can also provide the freedom to make choices that align with one's values and priorities. For example, an individual may choose to take a lower-paying job that offers more fulfillment, or a business may choose to invest in sustainable practices that align with their mission.

Increased Bargaining Power

Whether it's negotiating a lower price on a large purchase or securing better loan terms, having a strong cash position can make it easier to achieve desired outcomes.

It can also provide cushion in negotiations and reduce the pressure to accept unfavorable terms. This can lead to better outcomes and more favorable agreements over the long term.

The Cons of Holding Too Much Cash

Now that we’ve reviewed possible benefits to having excess cash on hand, there are also some drawbacks to consider. Below, we’re sharing a few potential downsides.

Inflation and Loss of Purchasing Power

One of the biggest risks associated with holding excess cash is the potential for inflation to erode its value over time. As prices rise, the purchasing power of cash can decrease, meaning that holding onto too much cash can actually result in a net loss over the long term.

For example, if an individual holds onto $10,000 in cash for 10 years, and inflation averages 2% per year during that time, the purchasing power of that $10,000 will have decreased to approximately $8,166. This means that even though the individual still has $10,000 in cash, they can only buy goods and services that are worth $8,166 in today's dollars.

Opportunity Cost of Uninvested Cash

While some level of cash reserves can be advantageous, holding onto too much can mean missing out on potentially higher returns available through investing in stocks, mutual funds, or other assets.

For example, if an individual holds onto $50,000 in cash instead of investing it in a diversified portfolio of stocks and/or bonds, they may miss out on potential returns of 7-10% per year, depending on market conditions. Over a 10-year period, this could mean missing out on hundreds of thousands of dollars in potential investment gains.

Potential Mismanagement and Overspending

Finally, holding onto excess cash can potentially lead to poor financial decisions or overspending. Without a plan in place for how to allocate funds, individuals or businesses may be more prone to impulse purchases or other financial missteps.

For example, if an individual receives a large windfall of cash and decides to keep it all in cash without a plan for how to use it, they may be more likely to overspend or make poor financial decisions. Similarly, if a business has excess cash on hand and doesn't have a clear plan for how to allocate it, they may be more likely to make unnecessary purchases or investments that don't align with their long-term goals.

While holding onto excess cash can provide a sense of security and stability, it's important to consider the potential downsides and risks associated with doing so. By carefully evaluating your financial goals and needs, and developing a clear plan for how to allocate your assets, you can make more informed decisions about how much cash to hold onto and how to invest the rest.

Striking the Right Balance

So how can individuals and businesses determine the right amount of cash to hold?

It ultimately comes down to assessing financial goals and needs, along with considering the aforementioned pros and cons. Your financial advisor can help you think through what the best course of action is based on your unique situation and goals.

Below are a few strategies to keep in mind.

Assessing Your Financial Goals

The first step in finding the right balance of cash reserves is to assess personal or business financial goals. Individuals and businesses should consider what short-term and long-term financial needs they have, as well as what objectives they hope to achieve with their funds.

Diversifying Your Assets

One strategy for managing cash holdings is to diversify assets across different types of investments.

For individuals, this could mean investing in stocks, bonds, or real estate alongside cash reserves. For businesses, diversification could involve investing in new products or services, or exploring alternative revenue streams to supplement cash holdings.

Regularly Reviewing Your Cash Position

Finally, it's important for individuals and businesses alike to regularly review cash holdings and assess whether they're maintaining the right balance.

This could involve setting up regular financial planning meetings, or working with a financial advisor to establish a long-term strategy for managing assets and cash reserves.

Conclusion

There's no one right answer to the question of whether holding too much cash is a bad thing. For some individuals and businesses, larger cash reserves may provide a sense of security and flexibility that aligns well with their financial goals. For others, maintaining a smaller cash position in favor of other investments or assets may prove more beneficial.

That’s why we go through the complete Financial Life Planning process with each of our clients. We learn about their unique circumstances, desires, and challenges to help decide what is best for them.

ABOUT TRIUNE FINANCIAL PARTNERS

Triune Financial Partners is committed to empowering people with life-changing financial counsel. Triune is an independent firm that values clarity, simplicity, and transparency. We're a fiduciary, which means we always put our clients' interests first. In addition to Financial Life Planning for individuals and families, we also serve 100+ businesses, churches and nonprofits to craft powerful 401(k) and 403(b) plans for their organizations. Whether you're working with one of our Financial Life Planners or setting up a 401(k) plan for your organization, Triune is here to help you thrive financially.

Interested in working with us? Get in touch here.

How to Stick to Your Financial Goals

It's not enough to set just any goals or pick random numbers and hope for the best. You need to set goals that are realistic and achievable (but hopefully a little aspirational as well)! Learn how to do that in this blog.

You know you need to have financial goals, but you’re not sure where to begin.

Even when you have goals, it can be challenging to follow through with them, leading many to give up.

In this blog, we’ll share tips on how to set and achieve financial goals based on our decades of experience working with clients.

How To Set Financial Goals

It's not enough to set just any goals or pick random numbers and hope for the best. You need to set goals that are realistic and achievable (but hopefully a little aspirational as well)!

Below are some questions you should ask yourself and tips to keep in mind to help you set effective and attainable financial goals:

What’s Your Current Financial Situation?

Before setting any financial goal, you must first understand where you stand financially. This means taking a careful look at your income, expenses, assets, liabilities, and credit score.

For instance, if you have a lot of debt, it may not be realistic to set a goal of saving for a down payment on a house until you've paid off most of your higher interest debt. Of course, this depends on your unique situation and goals, but this is why understanding your current financial situation is an important step to goal-setting.

Read More: How To Create a Debt Payoff Plan

What Do You Want to Accomplish in 5 Years, 10 Years, and Beyond?

Having long-term financial goals is vital in ensuring that you achieve financial stability in the long run. Identify the primary objectives you want to achieve and break them down into smaller, achievable steps.